35% of respondents have no savings – Ghana Earnings & Savings Survey 2

The success of GESS led to the launch of GESS 2 in May 2024. With over 600 respondents and the analytical chops of Alfred, we are happy to present the results in this report.

In 2023 CediTalk launched the Ghana Earnings and Savings Survey (GESS), a survey aimed at gathering data on the incomes and savings levels of people working in Ghana. With assistance from Data Scientist and Economist, Alfred Appiah, the results of the survey were published in June 2023, and have gone on to drive a lot of conversation on compensation levels, income inequality, and economic vulnerability.

The success of GESS led to the launch of GESS 2 in May 2024. With over 600 respondents and the analytical chops of Alfred, we are happy to present the results in this report. We hope you will find the information useful and support the initiative by sharing this post as widely as possible. As usual, we will share the raw data to the public to allow for researchers, policy makers, academics, the media, and civil society to also carry out studies on them.

- Advertisement -

Survey Design and Limitations

- Advertisement -

We chose to prioritize data comparability above all other objectives, which is why the research instrument remains almost identical to that of GESS 1. Only two modifications were made: the inclusion of a question about the length of time a respondent has been working and another about the primary currency in which the respondent earns. For those unfamiliar with GESS, I will explain the methodology below. Those already acquainted with it may skip the rest of this section.

The survey begins by collecting demographic information, including Nationality, Age, Marital Status, Number of Dependents, Gender, Employment Type, Education, Region of Residence, Number of Years Worked, Industry, and Primary Currency of Earnings. It’s important to highlight that while the survey focuses on individuals residing in Ghana, participation is not limited to Ghanaians.

Income levels were measured using ten categories, ranging from GH¢1,000 and below to GH¢50,000 and above. This income assessment aimed to capture all forms of earnings, including salaries, allowances, side gigs, and business profits. This comprehensive approach helps participants gauge how their total monthly earnings compare with their peers, rather than just their salary. It also ensures that self-employed individuals, entrepreneurs, and those in the informal sector can take part. Additionally, many formally employed individuals supplement their income with side activities that make up a significant portion of their earnings. Excluding these would lead to an underestimation of income levels.

Regarding savings, two metrics were used: a relative measure and an objective measure. The relative measure asked, “How many months’ worth of expenses do you have saved up?” This was designed to assess how long individuals could sustain themselves on their current savings without external assistance if they were to lose their income. This measure is considered relative because the same amount of money—say GH¢20,000—might cover 10 months of expenses for one person but only two months for someone else. The results from this metric allow participants to compare their financial buffer with that of their peers.

The other measure of savings was an objective cedi value, captured through the question: “Including your retirement benefits but excluding any physical assets, how much do you have saved up?” Retirement balances, such as Provident Fund balances, Tier 2 Pension balances, or other pension arrangements, were included because focusing solely on bank balances or investment accounts would be misleading. Pension funds often represent the majority of a formal employee’s savings, and excluding them could give the false impression that formal and informal workers have similar savings levels, which is often far from the truth. Physical assets were excluded because their cedi value is subjective and could skew the results. However, recognizing that physical assets are also an important measure of wealth, the survey concludes by asking about home ownership and car ownership.

Sampling Bias and Limitations

Since the survey was conducted online, the demographic skewed towards young, unmarried, graduate men living in Accra, aged 26 to 35. This makes the sample less representative of the overall working population. However, this does not diminish the survey’s value. By using cross-tabulation, we can categorize respondents based on their demographic profiles, allowing for more accurate comparisons among similar groups.

After the release of GESS 1, we were encouraged to consider weighting the data with population statistics in order to make it more representative. However, CediTalk’s objective is to present the data in as simple an approach as possible and to pique the interest of researchers for deeper analysis. That is why we make the raw data available to the public.

The survey was entirely anonymous, making it impossible to trace individual respondents. This also means that a respondent could potentially have completed the survey more than once, as no unique identifiers were collected. However, we are confident of the integrity of this data to the extent that this method of collection allows.

Demographic Profile

Now that we have touched on the academic sections, let’s jump into the results. We begin with the demographic profile of respondents.

GESS 2.1: Demographic Profile of Respondents

The respondents of the survey are predominantly young men between the ages of 26 and 35 (72%), with most of them unmarried (72%). About two-thirds (72%) are male, and the majority have either a graduate (59.1%) or post-graduate (32.4%) level of education. Most respondents live in the Greater Accra region (80.7%) and have 1-3 dependents (47.1%). A notable portion (40.4%) of respondents reported having no dependents at all. Female representation is relatively low at 26.7%.

Other important demographic data is that 81.6% of respondents are formally employed, 8.1% are self-employed, and 7.4% are informally employed. 37.2% have been working for 4-7 years, 27% have been working for 1-3 years, 22% have been working for 8-12 years, and 13.8% have been working for over 12 years. 87.4% of respondents primarily earn in Ghana cedis while a sizeable 10.3% earn in US dollars.

GESS 2.2: Which Industries do Respondents work in?

Most of the survey respondents work in a variety of industries, with 21% in the “Other” category. Financial services, including management consulting, audit, and assurance, account for 18%, while 15% are in the technology and telecommunications sector. Around 9% work in health and another 9% in mining, oil, gas, and energy. Education employs 8%, with 7% in non-profits and civil society. Smaller percentages are in construction (4%), communications (4%), government and politics (4%), and trade in goods (2%).

Earnings

Figure GESS 2.3 presents the overall earnings picture and shows that the majority of respondents (24%) earn between GH¢2,500 and GH¢4,999 a month from all their income generating activities including employment, business, investment, and so on. Overall, 55% of respondents earned over GH¢5,000 a month.

GESS 2.3: Overall Earnings

Let us dig into the distribution of income by each demographic as presented in Figure GESS 2.4. The majority of respondents earning less than GH¢5,000 per month are younger (81.4% of those 25 and under) and unmarried (52.9%). Those with a high school education or below are most likely to fall into this income bracket (79.4%). Interestingly, at this income level, there is minimal gender difference, with 45.1% of women and 45.0% of men earning below GH¢5,000.

Figure GESS 2.4: Monthly Income by Demographics

When we look at higher earners, the benefits of advanced education become clear. Among respondents with postgraduate degrees, 18.1% earn GH¢20,000 or more, compared to just 5.9% of those with a high school education and 11.6% of those with professional certifications. Even compared to graduates with a first degree, where 12.7% earn GH¢20,000 or more, postgraduate degree holders are far more likely to be in the top income bracket.

For those earning between GH¢10,000 and GH¢19,999, 30.7% of postgraduates fall into this category, compared to 22.3% of graduates, reinforcing the idea that advanced degrees open up higher-paying opportunities. Furthermore, individuals with more dependents tend to earn more, with 24.7% of respondents with four or more dependents earning over GH¢20,000, suggesting they are more established professionals.

It is worth noting that women make up only 26.7% of the survey sample, indicating an underrepresentation of women in these professional spaces to begin with. However, once women reach these levels, there doesn’t appear to be a significant gender disparity in the higher income brackets—11% of women and 13.3% of men earn GH¢20,000 or more. This suggests that while fewer women are in these roles, those who are present compete on relatively equal terms with their male counterparts in terms of income.

GESS 2.5: Earnings Levels for Ghana-Based vs Foreign-Based

As expected, 47% of Ghanaians who earn their income from foreign-based companies make over GH¢20,000 a month, compared to only 7% of respondents who work for Ghana-based companies. In fact, more Ghanaians working for foreign companies earn over GH¢20,000 a month than the percentage of those earning over GH¢10,000 from Ghana-based companies. This highlights a significant income advantage for individuals working with international companies, likely due to higher pay scales and favorable exchange rates. Please note that those earning income from foreign-based countries made up only 14% of the sample.

GESS 2.6: Earnings Levels for Public vs Private Sector

People working in the private sector tend to earn more than those in the public sector. In the private sector, 16% of respondents earn over GH¢20,000 a month, while only 5% of public sector workers hit that level. Meanwhile, 43% of private sector workers earn less than GH¢5,000 compared to 47% of public sector workers in the same income range. There’s also a bigger middle-income group in the public sector, with 26% earning between GH¢5,000 and GH¢9,999, compared to 19% in the private sector.

GESS 2.7: Monthly Income by top Industries of Employment

Figure GESS 2.7 shows how income varies across different industries. In financial services, 37% of respondents earn less than GH¢5,000, but 14% make over GH¢20,000. In the health sector, 43% earn less than GH¢5,000, and only 2% make over GH¢20,000. The mining, oil, and gas industry shows the highest earnings, with 30% of respondents earning over GH¢20,000, and only 20% making less than GH¢5,000. In technology and telecommunications, 29% earn less than GH¢5,000, but 24% earn over GH¢20,000. This suggests that mining and tech-related industries tend to offer higher-paying jobs.

GESS 2.8: Monthly income by Years of Experience

- Advertisement -

Figure GESS 2.8 highlights the relationship between years of experience and income levels. It shows that early-career workers (less than a year) overwhelmingly earn less than GH₵5,000, but income increases with experience. By 4-7 years of experience, there’s a more even spread across income brackets, with a notable rise in those earning GH₵10,000 or more. For those with over 13 years of experience, a significant 68% earn GH₵10,000 or more, with only 14% earning under GH₵5,000. The data reflects a clear progression in income as work experience grows.

Savings

Let’s begin the analysis of savings levels by looking at a measure of economic vulnerability – how many months an individual can afford their current consumption level were they to lose their source of income. Figure GESS 2.9 indicates that most respondents have little in savings. About 35% have no savings at all, and another 30% have only 1 to 3 months’ worth of expenses saved up. Only 12% have saved enough to cover more than 12 months of expenses, while 7% have 8 to 12 months’ worth of savings. A smaller portion (15%) has managed to save between 4 and 7 months of expenses. Overall, most people have less than four months of expenses saved up, indicating limited financial buffers for many.

GESS 2.9: Months of Expenditure Saved

GESS 2.10: Savings vs Income

Figure GESS 2.10 shows that people earning less than GH¢5,000 per month are struggling with savings—54% have no savings at all, and only 4% have saved more than 12 months of expenses. As income increases, so does the ability to save. For those earning between GH¢5,000 and GH¢9,999, 43% have saved between 1-3 months of expenses, and 9% have more than 12 months saved. In the higher income brackets (GH¢20,000 and above), only 10% have no savings, while 36% have more than 12 months’ worth saved up, indicating a strong financial cushion among higher earners.

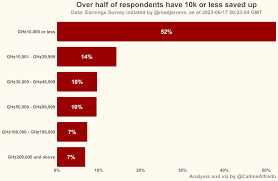

Now we can look at absolute amount of cedi values saved. Figure GESS 2.11 shows that 44% of respondents have GH¢10,000 or less saved up. A smaller group, 15%, have savings between GH¢10,001 and GH¢29,999. About 11% of respondents have between GH¢30,000 and GH¢49,999 saved, while 10% have between GH¢50,000 and GH¢99,999. Interestingly, 11% have saved GH¢200,000 or more, and 9% have between GH¢100,000 and GH¢199,999. This suggests that while most people have relatively modest savings, a small portion has accumulated significant financial reserves.

GESS 2.11: Cedi Savings Overall

GESS 2.12: Cedi Savings by Demographic

Younger respondents (25 and below) mostly have savings of GH¢10,000 or less (76.7%), while older respondents (35 and above) tend to have more savings, with 26.7% having over GH¢200,000 saved. Men generally have higher savings than women, with 11.5% of men saving over GH¢200,000 compared to 8.5% of women. Married respondents also tend to have more savings, with 21.2% having over GH¢200,000, while only 7.3% of unmarried individuals fall into that category.

People with fewer or no dependents tend to have lower savings, while those with four or more dependents are more likely to have higher savings, with 23.4% having over GH¢200,000 saved. In terms of education, the majority of those with only a high school education (79.4%) have savings of GH¢10,000 or less, while 20.1% of those with postgraduate degrees have savings over GH¢200,000.

GESS 2.13: Savings by Years of Work Experience

For those with less than a year of experience, 95% have GH₵10,000 or less saved up. Savings grow with experience, as only 21% of those with over 13 years of experience have less than GH₵10,000 in savings, while 37% have more than GH₵200,000 in savings. The data shows a clear link between years of experience and higher savings levels. This can partly be explained by the fact that people who have worked longer have managed to accumulate a larger balance in their pension funds apart from their personal portfolio investments.

Car Ownership

35.5% of respondents in GESS 2 owned cars. This has given us a great opportunity to identify the income levels at which people are likely to own cars. One reason why this has become important is because vehicle prices have shot up significantly in Ghana since 2022. You can read about reasons for the explosion in car prices here, but for now know that car ownership has become even more aspirational for the ordinary Ghanaian as prices have risen faster than incomes.

GESS 2.14: Car Ownership by Income

Car ownership is closely tied to income. Figure GESS 2.14 shows that among those earning less than GH¢5,000 a month, 88% do not own a car, while only 12% do. As income increases, so does car ownership. For those earning between GH¢5,000 and GH¢9,999, 38% own a car. In the GH¢10,000 to GH¢19,999 bracket, car ownership rises to 60%. Among the highest earners, those making GH¢20,000 and above, 74% own a car. This suggests that car ownership is largely found among higher-income individuals.

GESS 2.15: Car Ownership by Years of Work Experience

Figure GESS 2.15 shows how car ownership increases with experience. For those with less than a year of experience, 95% don’t own a car. By 8-12 years, 63% own cars, and for those with over 13 years of experience, 77% are car owners. It highlights the link between increased work experience and higher car ownership rates.

GESS 2.16: Car Ownership by Age

For young people who feel that everyone owns a car but them, please pay attention to Figure GESS 2.16. Car ownership is almost exclusively found among older people. Only 10% of people aged 25 and below own a car. Even among the 36-45 age group, 42% of them do not own cars. So do not allow the social pressure to get to you.

Home Ownership

Only 13.2% of the GESS 2 respondents owned homes, and that is understandable given the relatively young demographic of this survey. Therefore we will not go into much details about the homeownership statistics. We will only look at the relationship between homeownership and income levels.

GESS 2.17: Homeownership by Income Levels

GESS 2.17 illustrates home ownership by income group in Ghana. It shows that individuals earning less than GH₵5,000 have a very low home ownership rate (3%). As income increases, home ownership rises, with 18% of those earning GH₵10,000 – GH₵19,999 owning homes. For those earning GH₵20,000 and above, home ownership reaches 44%. This is not surprising as homeowners could typically be from socioeconomic classes that also offers them an opportunity to earn higher incomes. Also, at higher income levels, people are open to opportunities like mortgages that allow them to own houses at higher rates than lower income earners.

Downloading the Data

Please visit Alfred Appiah’s GitHub to download the raw data as well as all the beautiful charts I used and many more.

Referencing the Data

Our small request is that anyone who uses the data should cite it as the Ghana Earnings and Savings Survey, 2024 (GESS 2). This ensures consistency in naming that would make everyone be able to track how the data is used across different studies.

Supporting our Work

The entire study and analysis have been self-funded. We are currently not accepting donations so we only request that you share our work as widely as possible and do not reproduce it. You are however free to use the data to create whatever content you want as long as you reference Ghana Earnings and Savings Survey, 2024 (GESS 2) as the source.

Thanks!

Source:ceditalk.com

- Advertisement -