Bonds Are Back as a Hedge After Failing Investors for Years

Bonds would eventually erase much of their gains as stocks stabilized over the past few days, but the broader point — that fixed income worked as a hedge at a moment of market chaos — remains.

Gregg Abella, a money manager in New Jersey, wasn’t expecting the flood of phone calls he got from clients this past week. “Suddenly people are saying to us, ‘Wow, do you think it’s a good time for us to add bonds?’”

It’s something of a vindication for Abella. He’s been, in his words, “banging the gong” for bonds — and asset diversification, more broadly — for years. This was long a decidedly out-of-favor recommendation. Until, that is, stocks started to tumble this month. Quickly, demand for the safety of debt soared, driving 10-year Treasury yields at one point early last week to the lowest levels since mid-2023.

- Advertisement -

The rally has surprised many on Wall Street. The age-old relationship between equities and bonds — wherein fixed-income offsets losses when stocks slump — had been thrown in doubt in recent years. Especially in 2022, when that correlation totally collapsed as bonds failed to provide any protection at all amid the slide in stocks. (US government debt, in fact, posted its worst losses on record that year).

- Advertisement -

But whereas the selloff back then was triggered by an inflation outbreak and the Federal Reserve’s scramble to quell it by ratcheting up interest rates, this latest equities slump has been sparked in large part by fear the economy is slipping into a recession. Expectations for rate cuts, as a result, have mounted fast, and bonds do very well in that environment.

“Finally the reason for bonds is shining through,” said Abella, whose firm — Investment Partners Asset Management — oversees about $250 million including for wealthy Americans and nonprofits.

As the S&P 500 Index lost about 6% across the first three trading days of August, the Treasury market posted gains of almost 2%. That enabled investors with 60% of their assets in stocks and 40% in bonds — a once time-honored strategy for building a diversified portfolio with less volatility — to outperform one that merely held equities.

Bonds would eventually erase much of their gains as stocks stabilized over the past few days, but the broader point — that fixed income worked as a hedge at a moment of market chaos — remains.

“We’ve been buying government debt,” said George Curtis, a portfolio manager at TwentyFour Asset Management. Curtis actually first began adding Treasury bonds months ago — both because of the higher yields they now offer and because he too has expected the old stock-bond relationship to return as inflation receded. “It’s there as a hedge,” he said.

Inverse Again

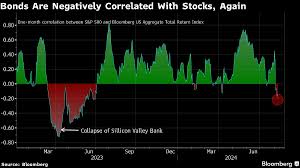

There’s another way to see that the traditional, inverse relationship between the two asset classes — which mostly held for the first couple decades of this century — is back, at least for now.

- Advertisement -

The one-month correlation between stocks and bonds last week reached the most negative since the aftermath of last year’s regional-bank crisis. A reading of 1 indicates the assets move in lockstep, while minus 1 suggests they move in the opposite direction. A year ago, it eclipsed 0.8, the highest since 1996, indicating bonds were practically useless as portfolio ballast.

The relationship was turned on its head as the Fed’s aggressive rate hikes beginning in March 2022 caused both markets to crater. The so-called 60/40 portfolio lost 17% that year, its worst performance since the global financial crisis in 2008.

Now the backdrop has shifted back in favor of bonds, with inflation more in check and the focus turning to a potential US recession at a time when yields are still well above their five-year average.

The coming week brings plenty of risk for bond bulls. July reports are due out on US producer and consumer prices and any sign of a resurgence in inflation could push yields back up. They already began ticking higher on Thursday after weekly jobless claims — a data point that’s suddenly gaining attention as recession concerns swirl — surprisingly fell, tempering signals that the labor market is weakening.

For all the excitement about bonds today, there are still lots of people like Bill Eigen who are leery of jumping back into the market.

Eigen, who manages the $10 billion JPMorgan Strategic Income Opportunities Fund, has held more than half of it in cash — mostly in money-market funds that invest in cash-equivalent assets such as Treasury bills —— for the past few years. At just over 5%, short-term T-bills yield at least a full percentage point more than long-term bonds, and Eigen’s not convinced that inflation is truly tame enough nor the economy weak enough to merit the kind of Fed easing that would change that dynamic.

“The rate cuts are going to be small and incremental,” he said. “The biggest problem for bonds as a hedge is that we still have an inflationary environment.”

What Bloomberg Intelligence Says

“The yield curve tends to bull steepen going into a recession. The exceptionally brief uninversion of the 2-year/10-year Treasury curve on Aug. 5 could presage a bull-steepening trend that we expect to persist as the economy slows. Meanwhile, we think the equity/bond correlation may be normalizing.”

Source:norvanreports.com

- Advertisement -