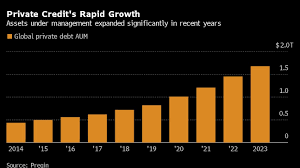

At a finance conference in London this summer, four senior investment bankers set about persuading the room that the $1.7-trillion private credit market isn’t a threat to Wall Street. Barely three months later, two of them have jumped ship to seek their fortunes in the upstart asset class.

Goldman Sachs Group Inc.’s Luke Gillam and Bank of America Corp.’s Murad Khaled, set to join AlbaCore Capital and Apollo Global Management, are the latest in a growing list of top bankers to make the leap. The brain drain is yet more evidence of private capital firms’ emergence as an enduring threat to banking’s traditional dominance of the lucrative corporate loan market.

At least 20 senior bankers in Europe — Gillam and Khaled among them — have switched sides since rate rises upended capital markets, according to rough estimates by Bloomberg News, as the continent’s less developed private-capital industry plays catchup with the US. But even across the Atlantic, where the trend has been evident for longer, a string of marquee leveraged-finance names such as Barclays Plc’s Tom Blouin has joined the exodus lately.

“We’ve seen a change in the appetite for larger private credit — aka ‘mega’ — funds to hire from leveraged finance,” says Harry Oliver, a headhunter at Paragon Search Partners.

Many banks were hobbled over the past couple of years after providing billions of dollars of debt for company buyouts that they couldn’t get rid of when interest rates spiraled. Nimble private credit firms, who lend directly to companies rather than syndicating loans to a large group, stole in to grab a hefty chunk of the market. While Wall Street is reclaiming some prize deals, and froth is coming off the direct-lending frenzy, bankers are still defecting. The flow is accelerating in Europe. Wall Street is braced for more exits.

Bonus-starved bankers are being seduced by fat pay deals, often including a cut of a firm’s performance fees, and by the chance to work in a hot part of the market that offers more freedom than increasingly rule-bound investment banking, according to several people who’ve made the jump and spoke to Bloomberg on condition of anonymity. Fewer working hours is another draw.

“While there’s always been a supply of leveraged financiers keen on private credit fund moves, disappointing bank compensation packages in 2023” have made it easier to offer compelling salaries to the best candidates, Oliver says. Some are also dangling the prospect of equity, according to three people with knowledge of the situation, a route that has minted life-changing fortunes for pioneers who first made the break to direct lending.

In Europe, bankers have moved to leadership roles at Blackstone Inc. and AlbaCore, while credit hedge fund Sona has also been attracting talent. The region’s younger private capital industry offers a path to get ahead quicker. And firms there are just starting to compete on the juiciest deals.

In the US, meanwhile, more private credit funds have been ready to make senior hires, whereas in the past they targeted junior employees because they were easier to train, says Skye Lucas, a senior vice president at recruitment firm Selby Jennings. “All these teams are hiring and growing,” she says. “Strong talent is definitely sought after right now.”

Ties That Bind

Those with good connections to large buyout firms, the entities that rely on borrowed money when acquiring companies, are particularly in vogue. These ties can help direct lenders snatch away ever-bigger deals from bank rivals.

“Private credit is a relationship business,” says Aymen Mahmoud, managing partner and co-head of transactions at law firm McDermott Will & Emery. “Those bankers will have strong relationships with large private equity firms, so it makes a ton of sense for the private credit firms to hire them.”

Firms like Apollo and Ares Management Corp. have been muscling in for some time, offering companies the comfort of borrowing directly from one fund or a small group to avoid the uncertainty of doing it via a bank-led syndicate of lenders, where their debt is priced in volatile public markets.

They’ve clinched landmark deals in the past year, including a €4.5 billion ($5 billion) loan to back the buyout of classifieds company Adevinta ASA, but it’s getting harder to compete. Banks gave a strong signal this week that they’re in fighting mode, winning most of a coveted €10 billion deal to back a buyout of Sanofi SA’s consumer-health arm.

Private credit’s rise has been lauded by some for taking risky lending away from depositor-funded banks, although regulators are increasingly anxious about an opaque source of finance where loans are hard to sell — and to value. For ex-bankers, though, breaking free of the regulatory handcuffs imposed on banks since the collapse of Lehman Brothers is part of the appeal.

“In private credit, you give people a wider set of parameters to operate in, and you see more creativity. It’s the very definition of disruption,” says Mahmoud.

Former bankers say private credit lets financiers get nearer the action, instead of feeling like a cog in a machine. They’re also able to nab a greater share of any upside from deals, while bonuses in the City of London and Wall Street can vanish if there’s a mishap elsewhere in the bank.

One reason banks lose talent is because they’re unwilling to compete on pay in slower periods, people with knowledge of recent industry moves say. In good times, leveraged-finance bankers may make more than private credit peers, the same people add, but they’ve had a tough few years. A moribund period for M&A has left bankers to occupy themselves with refinancings instead, where fees are much lower.

Many escapees are seasoned veterans. Gillam worked at Goldman Sachs for more than two decades and was its head of credit-finance capital markets for Europe, the Middle East and Africa. Khaled was Bank of America’s head of leveraged-finance capital markets in the region. Barclays lost its co-head of global leveraged-finance syndicate, Stephen Smith, to John Aylward’s credit hedge fund Sona. And in the US, Charles Brockett, a 12-year Goldman Sachs staffer, was tapped by Silver Point Capital for its private credit business.

Blackstone has been busy. Morgan Stanley’s co-head of European leveraged-finance capital markets, Jane Bradshaw, and its global head of securitized-products trading, Dan Leiter, have both moved to senior roles at the private-capital behemoth, as well as Barclays’ Blouin. And the US firm has been snapping up some heavy Wall Street hitters, including Citigroup Inc.’s former global head of investment banking Tyler Dickson, who’s now leading client relations for Blackstone’s credit and insurance unit.

To some extent ex-bankers are following the path of some of private credit’s leading lights, many of whom came from Wall Street. HPS Investment Partners and Sixth Street Partners were founded by former Goldman Sachs executives. Others, like Khaled, have moved back and forth.

Banking Strikes Back

As signs of life return to the M&A market, and central bankers tentatively start to reverse course on interest-rate policy, investment banks have been fighting back harder against direct lenders’ recent ascendancy.

They’ve been offering lower pricing and bigger incentives to get companies to pick them instead. And they’ve had a few major wins this year, with the Sanofi deal coming after a $5 billion bank-led, leveraged-loan package to help finance KKR & Co.’s purchase of a stake in healthcare analytics company Cotiviti Inc.

Some industry participants also say the brain drain may be close to hitting a temporary limit — in the US more than in Europe’s less-developed market.

“It really accelerated during Covid and continued through early last year,” says Kevin Mahoney, managing partner and global head of alternatives at consulting firm Christoph Zeiss Partners Inc. “We do expect there to be another wave soon. However, many of the banks have already lost a significant number of their best leveraged-finance bankers to private credit firms.”

There are other signs too that private credit’s breakneck expansion is facing higher hurdles. The start of interest-rate cuts could make the floating-rate debt offered by direct lenders less attractive than fixed-rate, high-yield bonds sold by banks, and the industry is attracting more regulator scrutiny. At the same time, the threat of an economic slowdown is casting a shadow, threatening to stem the flow of deals and increasing the risk of borrower defaults.

Still, even private credit’s most vocal critics acknowledge that the asset class is here to stay. And as long as its upper echelon can dangle the promise of greater riches, ambitious financiers will be tempted.

“Long-term you will make more on the buyside than you will in investment banking,” the recruiter Lucas concludes.

Source:norvanreports.com